Listen to this blog

Businesses around the world need consistent and comparable financial information, regardless of where they operate. This is where the International Financial Reporting Standards (IFRS) come in. This naturally raises the question of what is IFRS and, more specifically, what is IFRS in accounting for professionals working across borders.

IFRS has become the common language of financial reporting worldwide, providing standardized financial reporting and enabling companies to present their financial position clearly to international investors.

This blog briefly covers IFRS, its objectives, components, importance, benefits, challenges, and the differences between IFRS and Indian Generally Accepted Accounting Principles (GAAP). It also explains why IFRS proficiency is essential for finance and accounting professionals.

What is IFRS?

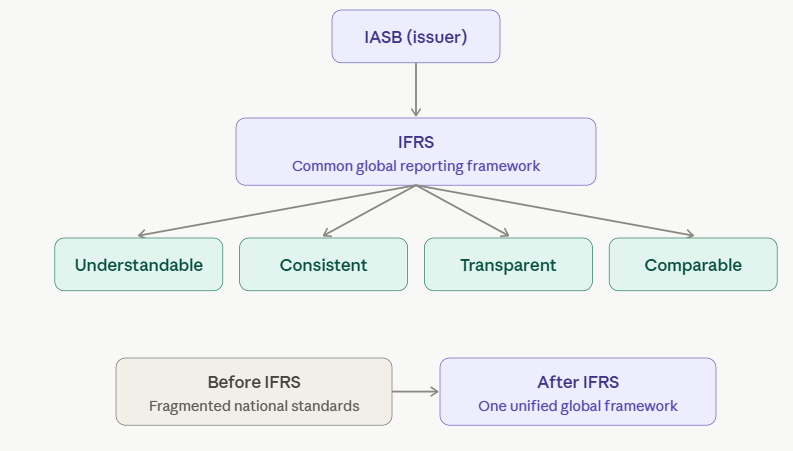

International Financial Reporting Standards (IFRS) are a collection of accounting regulations that the International Accounting Standards Board (IASB) develops and publishes to serve as a common global framework for the preparation and presentation of financial statements. This is essentially the answer to what is international financial reporting standard: a single rulebook meant to replace dozens of fragmented national systems.

Put simply, IFRS is a set of rules that financial statements must be understandable, consistent, transparent, and comparable even when they come from different countries.

Before implementing IFRS, countries had their own national accounting systems like Generally Accepted Accounting Principles (GAAP), which resulted in differences in financial reporting. The IFRS addresses the problem by unifying accounting practices globally.

What is the full form of IFRS?

Many learners searching for what is the full form of IFRS land here looking for a quick answer: IFRS stands for International Financial Reporting Standards. It is worth remembering this full form because the standards are frequently referred to only by the acronym in exam papers, job descriptions, and financial statements, so knowing exactly what the letters stand for is the first step to understanding the framework itself.

Who Issues IFRS?

IFRS standards are issued by the IFRS Foundation and the International Accounting Standards Board (IASB), an independent, non-profit organization located in London, United Kingdom. The IASB was set up in 2001 and took over from the International Accounting Standards Committee (IASC).

The IFRS Foundation oversees the IASB’s work and, together with it, is committed to the creation and use of the standards which are accepted worldwide. Understanding who issues these standards is part of understanding what is IFRS in accounting: it is not a government mandate but a globally coordinated professional framework.

Objectives of IFRS

IFRS’ main goal is to define a single set of high quality, consistent, and understandable accounting standards that are accepted globally and that help the financial markets become transparent, accountable, and efficient.

These are the main objectives of IFRS:

- Transparency: Used as a means to improve the comparability and trustworthiness of financial statements in different countries.

- Accountability: To support investors and other stakeholders in the correct assessment of company performance and financial position.

- Efficiency: To simplify and make the process of financial reporting less expensive for multinational companies.

- Global Consistency: Being the basis of the different theoretical concepts and practices worldwide, making the cross-border investments easier and more reliable.

Evolution and History of IFRS

IFRS evolution was marked by the foundation of the International Accounting Standards Committee (IASC) in 1973 that devised the International Accounting Standards (IAS). In 2001, the International Accounting Standards Board (IASB) came into existence and took over from IASC. IASB maintained the standards of the existing IAS and started releasing new standards under the name IFRS.

Timeline Highlights

- 1973: IASC is created.

- 1975 to 2000: 41 IAS standards are introduced.

- 2001: IASC was replaced by IASB and established IFRS.

- 2005: The European Union mandated IFRS obligatory for all listed companies.

- 2011: More than 100 countries adopted or converged with IFRS.

- Now: 169 jurisdictions require or permit the use of IFRS, according to IFRS Foundation data.

India has not fully adopted IFRS but has converged with it through Ind AS (Indian Accounting Standards).

Structure and Components of IFRS

IFRS comprises a Conceptual Framework along with the set of standards that regulate the preparation and presentation of financial statements.

Conceptual Framework of IFRS

The Conceptual Framework specifies the core principles that form the basis of IFRS. Besides, it helps accountants and policymakers.

Essential features are:

- Objective of Financial Statements: To provide the most valuable financial information for making decisions.

- Qualitative Characteristics: Relevance, faithful representation, comparability, verifiability, timeliness, and understandability.

- Elements of Financial Statements: Assets, liabilities, equity, income, and expenses.

- Recognition and Measurement: Features for recognizing and measuring these elements.

An Interesting Read: Step-by-Step Guide on How to Become a Chartered Accountant (CA)

Major IFRS Standards

Some of the most widely used IFRS standards include:

| Standard | Title / Focus Area |

| IFRS 1 | First time Adoption of IFRS |

| IFRS 2 | Share Based Payment |

| IFRS 3 | Business Combinations |

| IFRS 5 | Non-current Assets Held for Sale and Discontinued Operations |

| IFRS 7 | Financial Instruments: Disclosures |

| IFRS 9 | Financial Instruments |

| IFRS 10 | Consolidated Financial Statements |

| IFRS 15 | Revenue from Contracts with Customers |

| IFRS 16 | Leases |

| IFRS 17 | Insurance Contracts |

Additionally, older IAS standards like IAS 1 (Presentation of Financial Statements) and IAS 2 (Inventories) remain valid and form part of the IFRS framework.

Importance of IFRS in Global Accounting

The use of IFRS has changed the way global financial reporting is done. Its significance is made clear by a few points:

a. Global Comparability

The use of IFRS enables investors and regulatory authorities to compare the financial statements of companies in different countries, thus transparency is enhanced and the confusion arising from different accounting standards is reduced.

b. Attracting Global Investments

Investors operating worldwide will go for a company that reports under IFRS as it provides them with stability and trustworthiness. Consequently, an investor will be more comfortable when the firm complies with IFRS, and such a scenario can lead to an influx of foreign investments.

c. Simplifying Cross border Mergers and Acquisitions

Using a single framework for accounting makes it less complicated to do the necessary steps for the purchase or merger of the companies, such as due diligence, valuation, and merger processes.

d. Improved Financial Reporting Quality

By implementing IFRS, companies are required to use fair value measurement and provide full disclosure, which in turn improves the overall quality of the financial statements and limits areas for manipulation.

e. Reducing Cost and Complexity

One set of financial statements can be made for a multinational company that follows IFRS and operates in different countries rather than separate reports for each jurisdiction, thus it saves both time and money.

IFRS vs Indian GAAP (and Ind AS)

India is yet to fully adopt IFRS but has put in place Ind AS (Indian Accounting Standards) which are highly aligned with IFRS.

| Aspect | IFRS | Indian GAAP / Ind AS |

| Origin | Developed by IASB (Global Standard) | Developed by ICAI and Ministry of Corporate Affairs (MCA) |

| Approach | Principles based | Rules based (GAAP); Principles based (Ind AS) |

| Fair Value Concept | Widely used | Partially adopted under Ind AS |

| Scope | Global use | Indian use with IFRS convergence |

| Reporting Entities | Listed companies in IFRS adopted countries | Indian listed and large companies |

| Regulatory Body | IASB | Ministry of Corporate Affairs (MCA) and ICAI |

IFRS is the worldwide benchmark whereas Ind AS is India’s aligned version of IFRS that facilitates comparability with international reporting standards.

Benefits of Adopting IFRS

The benefits of IFRS are not limited to mere adherence to standards but rather, they represent a source of value that creates a positive cycle for companies, investors, and economies.

a. For Companies

● Improves global image and trustworthiness

● Decreases the costs related to the preparation of financial statements in multinational operations

● Attracts and facilitates the use of the international capital markets

● Enhances a company’s internal control system and decision-making process

b. For Investors

● Ensures that the information is clear to everyone and that it can be used for comparison between different countries

● Making investment decisions becomes easier

● Confidence keeps on growing which leads to less risk of losing money

c. For Governments and Regulators

● Helps to trace easily the financial transactions and activities of the company

● Makes national financial systems compatible with global standards

● It is relatively easy to monitor and enforce the corporate disclosure by the management

IFRS Adoption Around the Globe

As of 2026, IFRS Standards are required or permitted in 169 jurisdictions worldwide, according to IFRS Foundation data.

● Full adopters: European Union, Australia, Canada, South Africa, Singapore, and more.

● Partial adopters / Converged frameworks: India (Ind AS), China (ASBE), Japan, and the United States (US GAAP remains the domestic standard).

United States and IFRS

The U.S. continues to follow US GAAP (Generally Accepted Accounting Principles) rather than IFRS. The formal FASB-IASB convergence project that ran through the 2000s and early 2010s has effectively wound down; as of 2026, the two boards no longer run joint convergence projects, though their chairs continue informal quarterly discussions on select topics where standards still overlap, such as goodwill accounting.

India’s Case: Ind AS

India rolled out Ind AS (Indian Accounting Standards) which is very close to IFRS, in 2016. Market listed companies and big unlisted companies (with net worth above ₹250 crore) are mandated to present their accounts in compliance with Ind AS.

The Future of IFRS

IFRS is still changing as a result of the increasing worldwide interconnection. The changes will probably emphasize the following areas:

● Environmental, Social, and Governance (ESG) Disclosures and Sustainability Reporting

● Digitally Reporting through XBRL (eXtensible Business Reporting Language)

● Further Developments of the Standards on Cryptocurrency and Digital Assets

● Financial Systems Powered by AI Integration

A major next move towards providing globally comparable sustainability disclosures aligned with financial reporting is the creation of the International Sustainability Standards Board (ISSB) under the IFRS Foundation.

This is no longer just a future direction. As of 2026, the ISSB’s sustainability standards, IFRS S1 and IFRS S2, are already mandatory or formally adopted in more than 20 jurisdictions, together covering a majority of global GDP, with several more jurisdictions in active adoption processes.

Conclusion

The International Financial Reporting Standards (IFRS) have essentially changed the way companies communicate their economic results to the world market. By being transparent, consistent, and comparable, IFRS becomes a universal language of business that connects local financial systems with the global ones.

For anyone still asking what is IFRS or what is IFRS in accounting, the short answer is that it is the global rulebook that makes financial statements speak the same language everywhere. And for those still wondering what is the full form of IFRS, it is International Financial Reporting Standards, the very framework this blog has walked through.

First of all, implementing IFRS in companies increases their trust, investor confidence, and marketability in an international environment. Secondly, for professionals, grasping IFRS is like having a ticket for worldwide career moves in areas such as finance, auditing, and consulting.

The Online B.Com aligned with ACCA by Manipal Academy of Higher Education (MAHE) via Online Manipal is a program that impresses its worldwide relevance. It prepares students with a combination of scholastic knowledge and professional skills. The students become not only proficient in accounts, finance, and business administration but also get familiarized with the International Financial Reporting Standards (IFRS), which is the common language of the global business sphere.

India is progressively harmonizing its Ind AS structure with IFRS. Therefore, familiarity with these standards is not considered as a mere option, which is a must for anyone in the accounting and finance field who has the ambition to succeed in a tightly linked world.

Prepare for your next career milestone with us